China’s Economy Slowdown

The slowdown of China’s economy has been long time coming. The unprecedented level of growth over 2 decades made China the worlds second largest economy. Over the same period it has not lifted millions but hundreds of millions out of poverty and placed China as one of the key pillars of the global economic order.

You have to only look at prices of copper, coal and iron ore in the last 10 years to see its insatiable appetite for commodities. The demand fueled one of the largest commodity booms of our generation. We consider liquefied natural gas to be the next area that will benefit from China’s shift to cleaner energy sources.

It is undeniable that export led growth with the goal of becoming the worlds factory has the been the driving force for domestic employment and income growth. Chinese manufacturing at more competitive low labor costs has been the primary force in replacing manufacturing jobs in developed countries.

Manufacture Powerhouse – jobs are never coming back

Manufacturing companies in the west found that the key to survival is not compete with Chinese companies on basis of cost but move up the value chain but there is only so much space up on the value chain that can support domestic manufacturing without large jobs.

The political ramification in the shift in economic landscape has been long time coming. One of the key arguments for those that argued for United Kingdom to leave Eurozone is an independent Britain will have greater ability to bring back the lost manufacturing job losses.

These same arguments has been played out in the US in the rust belt during every election cycle where politicians promise to bring back the jobs that has been lost over the decades since the freeing up of the global trade regimes.

Reality is that these jobs are never coming back. For example the loss of US steel manufacturing in the rust belt states can be partially attributed to more free movements of goods and less protectionist tariffs. But those also overlook the shift in the production from the mid west to the coastal cities.

Simply there was a shift in steel product not just overseas but also within the United States. While the rust belt felt the full force of plant closures, on the other side was coastal cities which benefited from investment in better and competitive production processes.

In the instance of the UK it is not the the French, German or Italian producers that ate UK’s production base. Rather the blue collar and middle classes in these countries are in the same boat. The shift in jobs has been from developed countries to China. The genie has came out of the bottle and there is no going back.

Currency of China (Chinese Yuan)

Most developed economies currencies are under free float regimes. This means the daily Aus Dollar, Yen per USD or Canadian dollar exchange rates are set by the market participants based on expectation of economic growth, future inflation, unemployment rates and risk sentiment.

The Chinese Yuan exchange rate on other hand is under managed float regime. A managed FX rate means the Chinese central bank, the People’s Bank of China (PBC) sets the daily CNY verses US dollar exchange rate.

The initial competitive advantage China had over the Western economies was its low cost of labor. Overtime as the economy became more developed. The exchange rate started to play a greater role in keeping the economy competitive and under pressure from other countries, PBC started to strengthen the currency.

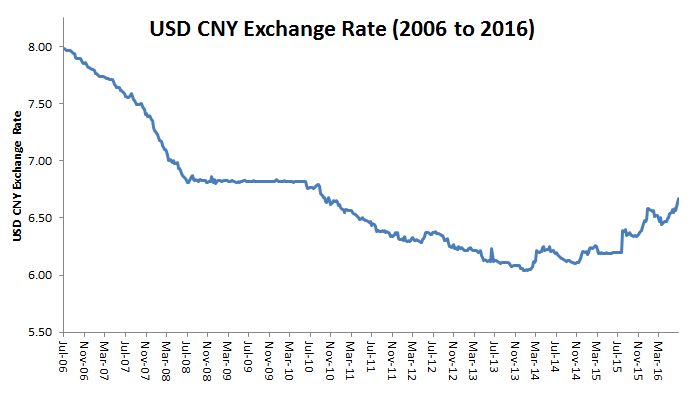

USD to RMB Forecast

The chart above shows the USD CNY exchange rate over the last 10 years. It is unmistakable the central bank was managing a gradual appreciation of USD verse CNY rate from 8 to 6.25 per USD from 2006 to 2014.

Important to note the that the US dollar index depreciated significantly following the Federal Reserve cutting interest rates repeatedly in response to the financial crise. During the crises PBC kept the CNY exchange rate fixed against USD from mid 2007 to 2010.

The guided appreciation and corresponding fall in the US dollar meant that the net volatility in exchange was limited. Also by pegging against the US dollar when it was in freefall within a wider economic context the yuan also depreciated significantly against the Japanese Yen and Euro.

As the economy slowed nearing end of 2013, PBC reversed the previous trend and commenced to depreciate the daily USD CNY FIX.

This has become the prevailing trend for the RMB verses the US exchange rate.

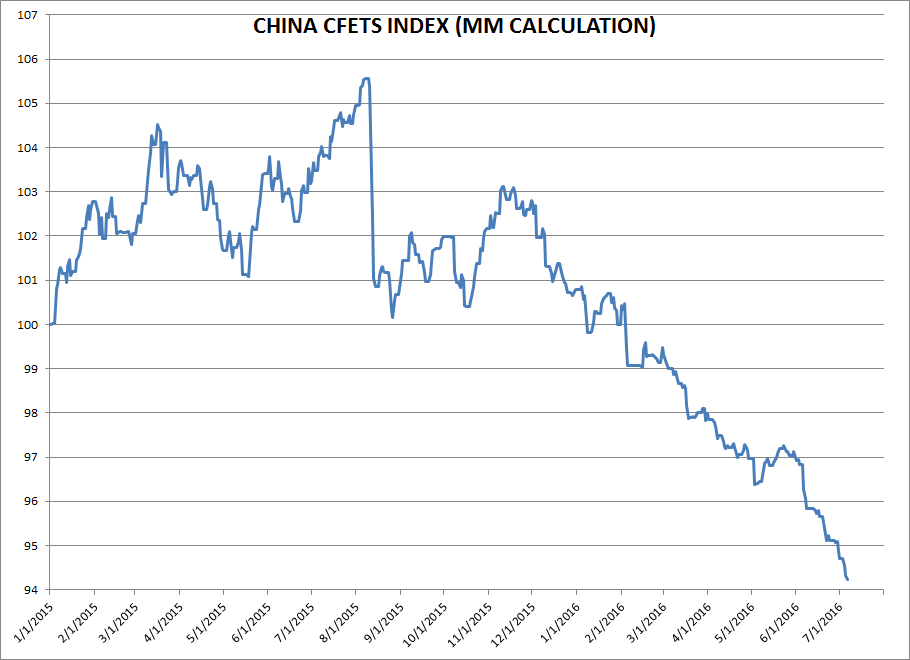

China Yuan Index – CFETS RMB Index (China Foreign Exchange Trade System)

PBC announced a new benchmark from December 2015 onward which represent the primary benchmark where the RMB exchange rate will be pegged against.

The CFETS index is a trade weighted 13 currency index and is designed to shift the focus away from the CNY USD peg with associated political pressure from US treasury and emphasis a clearer representation of the exchange against all the major trading partners.

The table below shows the composition of the CFETS index and the weight of the individual currencies. The Hong Kong dollar is pegged verses the US dollar. Therefore the US dollar make up more than 30% of the new RMB currency benchmark.

[etable caption=”” width=”500″ colwidth=”75|75|50″ colalign=”left|left|center|left|right”]

FX,Weight

USD,26.4%

EUR,21.4%

JPY,14.7%

HKD,6.6%

AUD,6.3%

MYR,4.7%

RUB,4.4%

GBP,3.9%

SGD,3.8%

THB,3.3%

CAD,2.5%

CHF,1.5%

NZD,0.7%

Total,100%

[/etable]

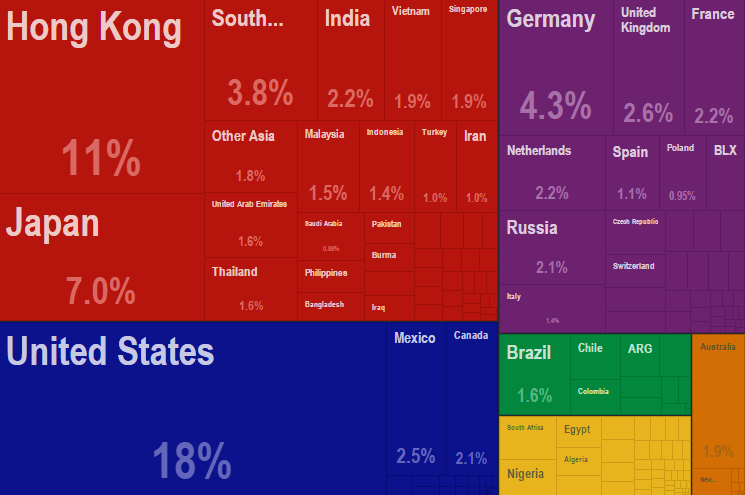

Destination of Chinese Exports

Heat map below highlights the destination and weight of the Chinese exports to the rest of the world. The slight variation in the basket % and the actual export could be attributed to timing as most recent data from MIT is up to 2014.

Source: MIT

One of our favorite blogs has calculated the CFETS index 12 month prior and post implementation performance. It is clear from the chart that the CNY has depreciated against a trade weighted basket of currencies.

The trend is clearly down and we see expect further downside in the exchange rate.

Key factors driving Yuan devaluation

It is clear the People’s Bank of China goal for CNY USD is to continue the devaluation trend. The current growth policy that brought China out of poverty look to have reached its limits. The bulk of the shift of production, hence jobs from the West to China seems to be completed where future movements will only have marginal impact as global supply chains search for even cheaper destination to manufacture goods.

Economy in transition

China’s services sector will be the source of growth for the next leg of its industrialization. The key risk is like the developed countries the size of the services sector will not make up the losses in manufacturing. Hence by maintaining a weak currency it would keep its economy and cost structure more competitive against other low cost countries and limit impact of its own job stream of losses.

Lack of political will for reform

We see political system to be a headwind for the economy going forward.

The last 10 years can be characterized as the lost decade of economic reform. Beijing has avoided major economic reforms in the social system, financial, housing or health care. The structural issues the country face is not going away either.

Now with the days of 7% year on year GDP growth behind them. Xi Jing Ping has primarily focused on consolidation of political power under the guise of corruption crackdown.

Dangerous banking sector

The banking system is still shackled with a dangerous level of non performing loans due to the stimulus implemented to tackle the last financial crises. A closed financial system where the there are limited long term investment opportunities means real estate is the only game in town for long term wealth creation. The level of wealth management products looks to be a systemic risk to the system.

It is no wonder that those that have the means are looking to move capital out of the country. The recent outflow of funds out of China have pushed house and apartment prices in Sydney and Vancouver to record territory.

Given the clear risk factors above we are cautious on the Chinese Yuan. At the end of the day unlike like our other currency forecasts where the future is dependent on market responses and expectations on the trend of economic growth. The future CNY rate will be a political choice and implemented by the PBC.