The currency has depreciated significantly since April 2013 when the Australian dollar peaked at 1.10 against the US dollar. The decline in value of the currency matches the decline in price Australia’s key export commodities from Iron Ore, Coal to Copper.

Aside from the fall in commodity prices, another major driver of depreciation is the Reserve Bank of Australia (RBA) talking down of the value of the currency as they see the value of the AUD too high relative to the fundamentals of the Australian economy. This is reinforced by the continuous cuts in interest rates and negative sentiment in the market on the future growth of the Chinese economy.

Important: read our note on the Impact of Brexit on GBP and potential contagion risk spreading to EUR.

Australian is an open economy with a free floating exchange rate, this means the government aside from the occasional RBA policy communication does not control the value of the exchange rate. During the commodity boom the value of key export commodities priced in US dollars were the key driver in pushing up the Australian dollar as the proceed from commodity sales are converted back to Australian dollars.

It was unavoidable that the currency overshot to the upside when the commodity boom was in full swing. We see weaken AUD will act as a stabilization mechanism for the economy in the post boom period.

However the FX market can undershoot the downside after boom just like it overshot the upside during the commodity. Key risk for the economy going forward would be the real estate sector where we are especially cautious given the upcoming supply. Our Sydney property forecast sees 2018 as a major year for the real estate sector while Brisbane apartment market and Melbourne can be considered already oversupplied. Government has stepped in exacerbating potential slowdown by introducing additional stamp duty for foreign investors.

Aussie Dollar to US Performance

The current level where the currency is trading at near 75 cents Aus Dollar to US is the level where we see margin risk and reward in betting for further currency depreciation. The negative sentiment on Chinese slowdown has become the consensus and we feel it has mostly been priced in the exchange rate. The bounce back in commodity prices in 2018 has supported the Aussie dollar rate in the medium term. The performance of the underlying economy measured by job creation and unemployment has has also been held up relatively well given the level of the price decline in the export key commodities.

From the US monetary policy perspective, the Federal Reserve delaying of interest rate hike to late 2016 and slower than expected rate rises in 2018 will continue to support the Aus Dollar to US exchange rate.

The broader private sector has seen limited negative effect from the end of the mining boom aside from the mining and sectors that indirectly benefited from the mining sector. There were no cascading or ripple affects across the broader economy. This is due to the fact that while commodities make up a significant portion in the total value of exports, it is capital intensive contrast to labor intensive manufacturing industry. The slow down in mining spend fell on capital expenditure rather than labor hires.

The fall in export income are primarily felt in pockets of labor market in mining heavy states like Western Australia and to a degree Queensland. Even in these states, the jobs during the boom were primarily construction rather than operational. The impact of the exchange rate on a segment basis is seen mostly damaging to listed miners and government revenue. This is offset by strong tourism and education markets like New South Wales and Victoria.

Population heavy states of New South Wales and Victoria are relatively unscathed and are actually outperforming by benefiting from lower Aussie to USD rate. The weak AUD provides an automatic stabiliser effect in boosting export heavy sector like tourism.

2018 Year to Date Performance

[visualizer id=”1585″]

It is important to note that the while local fundamentals can dictate the movements in the currency, wider factors that drive changes in the US dollar and market sentiment can also impact the Aus Dollar to US exchange rate.

Chart above shows the year to date performance of the Australian dollar against the major cross rate pairs.

AUD to Yen has the weakest cross rate performance year to date. The surprising strength of the Japanese yen has caught a large portion of the market offside. This could catch on BOJ announce additional monetary policy easing measures.

Aussie Dollar Prediction Drivers

The only certainty in markets is uncertainty and it is always difficult to forecast movements in exchange rates. There are some broader trends which could push the currency in a particular direction. Based on these economic trends we are positive on the Aus dollar to us based on a number of positive factors:

1. Broader economy are adjusting to lower exchange rate which will feed through to employment and income growth going forward. Low interest rates have limited job losses outside of mining and lower exchange rate have been a boom to tourism. Tourist industries are labor intensive industries contrast to mining which means the positive affects will be felt to a wider extent in states with large population.

2. Growth of new export products such as Liquefied Natural Gas will boost demand for AUD against USD. LNG will be the next export boom for the economy. The completion of construction of LNG trains means the spend on construction and contractor spend will fall which is offset by exports of LNG products. It is expected to ramp up in LNG will contribute materially to government tax revenues and private sector profits (our preference in the sector is Origin Energy).

Even with recent weak oil prices the pure increase in volume from the current base means it will be a significant positive for the Australian economy.

3. Slowdown in China is on everyone’s mind. We have been bearish on China since 2013 where the risks to debt fueled investment growth model could be seen as unsustainable. With the 30% fall in aus to us dollar exchange rate over a 2 year period. The extent of the slowdown has priced in the currency.

Although key commodity export prices has fallen significantly it is still above historical levels. We do not see commodity prices continue to fall to historical level ranges because demand from China has structurally changed the global demand profile across all commodity markets.

4. Second wave on demand for exports will focus on soft commodities like diary and meat as well as Education and Travel.

5. They key risk in our prediction is a weaker Chinese economic data. Recent developments out of China has soften our view on the economy in the rest of the year.

Highlights of major Australia exports trends

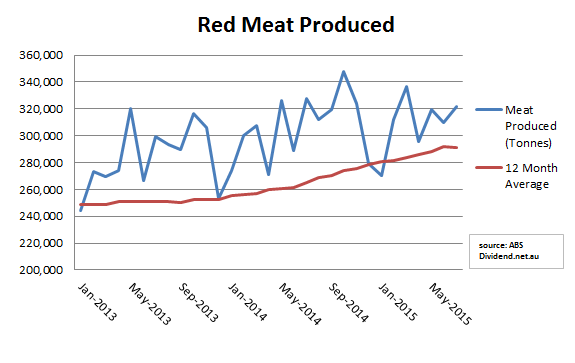

Chart below shows increase in meat production by primary producers since start of 2013. The monthly figures can be volatile but from looking at the 12 month average (red). It started to trend up from start of 2014.

This shows the decline in Aus dollar to US has supported the primary production industry. It has also increased competitiveness of meat producers in major export markets resulting in significant increase in prices.

Farmers has reacted accordingly with higher production (offset by drought in some areas). The increase in production is sold overseas as domestic meat price has not fallen inline with higher production.

Australian consumers have actually experienced higher prices as most increase in production are sold overseas and domestic consumers have to compete with export prices.

One advantage of strong meat production is increasing exports to our key market, the United States is it provides diversification of export from just reliant on the Asian markets.

Service Exports: Education

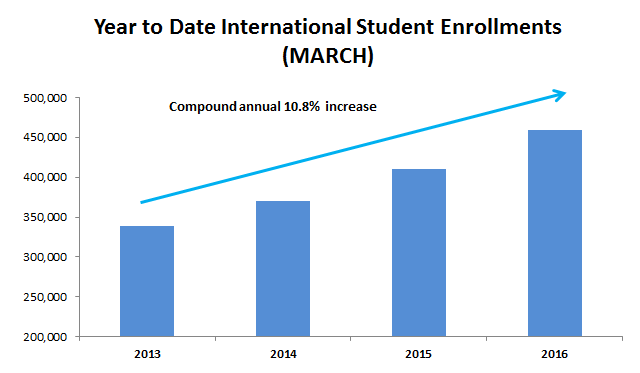

Education as an export is more sticky as consumers are reliant on reputation and quality of service rather than pure commodity products. The education export sector is the largest sector after the commodity sector.

Chart below shows the number of international student enrollments in Australia. Over the last 4 years, international student enrollment had a compound annual enrollment of 10.8%. We feel that while the service sector has been boosted by the decline in the exchange rate.

This is a positive for the long term economy as the export of education services whether secondary or tertiary is literally the export of knowledge, a service based product which is labor intensive.

The level of growth directly impact wages and employment across a number of segments of the economy verses capital intensive exports such as mining and agriculture where most of the inputs are imported.

Domestic and International Travel Travels

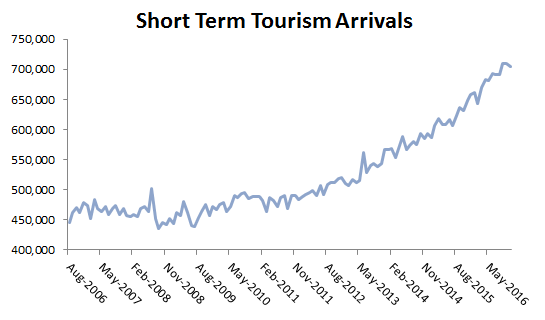

Chart above total inbound travelers over the last decade. The currency decline has been the backdrop on the changing habits of Australians and oversea visitor’s view of coming to Australia it is undeniable that the trend is heading up.

More than 30% decline in exchange rate is quite a move in FX markets. Since prices does not fall forever, the current weak commodity prices is priced in the current value of the Aussie Dollar to US dollar exchange. The AUD exchange rate could surprise on the upside as result of the snap back in commodity and energy prices. There comes a point where value comes into play. We are already seeing signs of strength in the iron ore market.

The question is if interest rates will stay for lower and longer or inter alia if future inflationary expectations pushes RBA to raise rates. Post GFC RBA was quick in picking up rates as China ramped up stimulus. This outcome could make our forecast largely correct to unmistakably wrong. Lower for longer rates could further dampen Australian Dollar Prediction and keep where it is today, it is a non zero probability event but not our base case.

Implication on Equity Portfolio from AUD/USD Forecast

We are market agnostic in running our investment portfolio but generally we like US stocks in our portfolio as it provides sector diversification and strong franchises we cannot have from the just ASX. This is because the ASX large cap index is heavily exposed to miners and financials.

As result of our Australia Dollar prediction that it will appreciate from where it is today. We have shifted our portfolio weight towards companies that have limited overseas exposure and are driven by the domestic market. Companies with overseas income will face headwinds as the Aussie dollar to US dollar appreciates.

Potential risk to further decline in Aussie Dollar to US

Residential Market

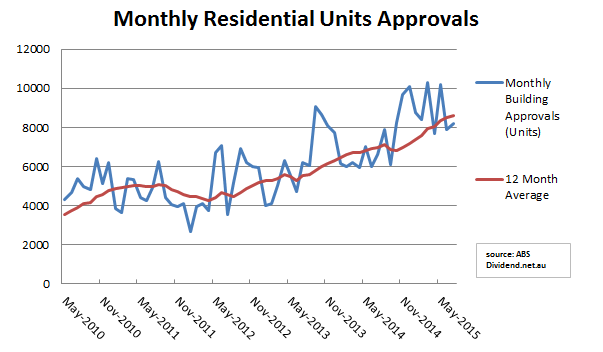

Building approvals has risen strongly on the back of interest rates falling to record low. The boom in residential construction across Sydney, Melbourne and Brisbane is primarily driven by residential units rather than standalone houses. Chart below shows the monthly residential unit approvals. Chart excludes standalone housing approvals as that trend has not changed over the same time.

One component driving the increase in unit approvals is the lagging supply during the previous decade. Household formation has gradually increased inline with GDP while the supply in meeting the demand has lagged materially. This current increase in building approvals can be seen as simply playing catch up. However with everything in markets, there is always a risk of overshoot. Overshooting in unit approvals will lead to pressure on house values further down the track as the trend reverses and there are too much apartment coming online verses demand.

ABS highlights the rise in house prices contributed to an increase in total average household wealth. Note the spread of wealth across the economy is more unequal verses income because of home ownership rates as only 2/3 of households owns or partly owns their home.

Average household wealth for those households who were renting was about 21% ($183,000). Owner occupied households with a mortgage ($857,900) and 13% of owner occupiers who owned their home outright ($1.4 million). Average household wealth for low wealth households in 2013–14 was $35,600, for middle wealth households was $462,500 and for high wealth households was $2.5 million. “

The risk to the economy from fall in house prices is heightened due to the high levels of home ownership. Ironically, home ownership has become pro-cyclical factor where price increases make the boom feel better but the impact of any slowdown will also be exacerbated across the economy. Any significant weakness in house price will be especially felt in the Australian Banks and on consumer spending.

The 4 pillars policy which result in the big 4 accounting for significant portion of the residential mortgage market means these institutions will no emerge from any crises unscathed. This is why we are cautious on the Australian banks irrespective of the Australian dollar forecast. Even Australia New Zealand Bank with its Asia exposure will not come out unscathed. In either scenario where if the exchange rate appreciates which mean it is driven by higher rates.

Residential housing market will be under pressure. Further decline in the Aussie dollar to US could be due to Chinese slowdown worse than feared. This is not positive for the Australian economy with flow on effects on the banking sector.

The upside is we do not see a US style housing collapse. The US housing market experienced once in a generation housing boom which the fallout is still being felt today. This is exemplified by the Fed maintain near zero interest rates 9 years after the bubble popped. Australian housing excess is not to the extent of the US boom but aggregate risk to the economy from any residential slowdown will negative impact the AUD.USD. This scenario is not in our 2018 Australian dollar forecast.

Other Australian Dollar Cross Rates

While we have primarily focused on the AUD/USD exchange rate. There will be wider implication on other major cross rates for the AUD. As all exchange rates are linked, changes in the main FX rate will have implication on the AUD to NZD Exchange rate as well as Aus dollar to Euro Exchange rate.