The downside of the recovery in equity market is there are limited opportunities to deploy capital at this level. Frankly we see the market as fully priced. The increase in volatility post UK EU referendum will create opportunities for those that are patience and willing to ride out the whipsaw.

In our Australian equity outlook, we identified that whilst there are pockets value. We are broadly neutral on the overall market. There will be positive returns but we are not sure if the risk is really worth the reward pre brexit voting result.

The benefits of being a multi asset class investor is that we can shift our focus to the area which present the greatest relative value given a unit of risk. As equity markets looking less attractive by the day we have shifted our focus to the FX market.

Our original US dollar forecast sees a pullback in the value of the US dollar in the medium term. While as we predict weakness in the dollar through exchange rate pair like the dollar yen. The euro dollar rate is one rate we are keenly watching. This year the Euro has rallied against the greenback to near 1.15 EUR USD. The UK referendum result has become the primary catalyst to short EUR USD position.

Our short Euro position is conditional on a number of factors:

1. BREXIT Contagion Risk Spread to Europe

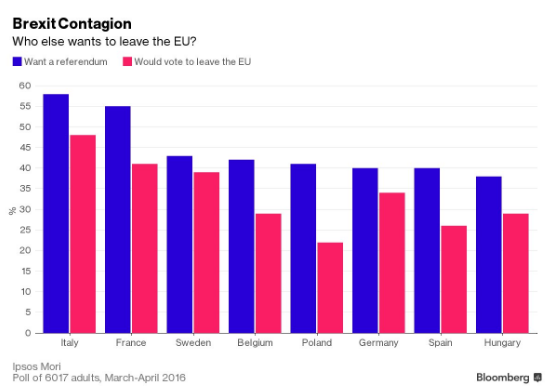

Poll above by country shows the political sentiment across the region.

The results of the UK referendum are in and Brexit is on! The UK voting to leave the EU is unmistakably shot across the bow of the 2nd largest economic bloc in the world. The risk to similar actions across the Eurozone region has increased considerably. While we were originally bullish on the GBP sterling lead up to the vote. We only changed our mind the last minute due to the close nature of the vote.

The aftermath financial market response shows the fragility of the current global financial system. Everything that is liquid is sold. The Euro sell off initially lagged the GBP selloff. We used the opportunity to sell more Euros as we see real contagion risk spreading across the Eurozone.

Any scenario where the major European economies like France or Italy holding its own referendum on the EU will make Grexit and Brexit risk like a bump in the road. Now there is a real precedent for the each countries nationalists.

It is important to understand while there are numerous economic arguments for the existence of the EU, ultimately the union is a political decision. From a political economy perspective, any negative economic consequence are result of leaving the economic bloc is a price paid for the political choice. Referendums are a function of political and economic choices.

2. European Economy

It is no secret that the Eurozone economies are not great. The recent lull in bad news does not mean the fundamentals have improved. We are cautious of ECB commitment on continually loosen monetary policy to support growth.

Our base case is that ECB will continue to provide a supportive monetary policy backdrop. Best case for shorting Euro is if the central bank ratchet up monetary support.

3. European Financials

On one hand there is the economy, on the other the European financial sector could add to the regions woes.

As Deutsche Bank recently caught the headlines, the Italian banks are even worse. We cannot rule out potential systemic risks the financial sector pose to the economy.

The risk of a next recession driven by a European credit crises is a very real possibility. In this event, dollar euro will not fare while. The odds are not huge, but is definitely higher than zero which the current exchange rate implies.

Examining these factors side by side shows that the US dollar is preferred against the Euro in many areas. In the instance where we have to choose between Euro vs US, we choose US dollar and are positioned accordingly in the portfolio.