This page is created to be a comprehensive definition of key terms used in Dividend Investing. It is a one stop FAQ on all main dividend terms, calculations, and how they operate.

Table of Contents

- Measuring dividends

- Everything about dividend payouts

- Different dividend dates

- All types of dividends

- How franking credits work

What is a Dividend?

Dividends are payments made by companies to their shareholders and represent the company’s profits up to that point in time.

Our analysis shows that dividends make up a large portion of the average stock market returns in the long run. Long term investors primarily use dividends as a source of passive income as experience shows companies are loath to cut dividends even during economic downturns.

A slight difference is seen from listed property trusts, which theoretically are not called dividends but distributions. This is because REITs are trusts and payout from trusts are distributions of the proceeds of the trust.

There are several ways to represent the relative value of dividends.

- The most common forms of this are in dollars, for example BHP declares $2 dividend per share.

- In some instances dividends can be quoted in a yield format like BHP is trading on a 3% dividend yield.

How to measure dividends?

Dividend per share

Dividend per share = total amount paid out / the number of shares outstanding.

Dividend yield

The dividend yield is a measurement of dividend payout in a yield and allows a comparison of the dividend rates with different share prices.

Dividend yield formula = dividend per share / share price

There are two main types of dividend yields:

Historical Dividend Yield – The dividend yield is based on the last 12 months of dividends.

Forecast Dividend Yield – The forecast dividend yield is calculated using the forecast dividends over the next 12 months divided by the share price. A common mistake investors make invest purely based on a shares high dividend yield thinking the company can maintain dividends. An example of this is investors buying bank shares after the market sell off during Covid-19 thinking the dividends will be untouched in the future.

How to Calculate Dividend Yield

The dividend yield is calculated by dividing the dividend per share by the trading price of the shares.

Dividend yield formula

Dividend / Share Price = Dividend Yield

Market convention uses the annual dividend yield where the amount is either over the last 12 months (historical) or next 12 months number from management guidance or the consensus analyst forecast. The yield shows investment income the investors would have received from owning the share on an annualized basis.

Like property rental yield, the dividend yield is an easy way to recognize how much income is generated by the investment. Investors should also be conscious of the dividend amount paid as a proportion of the earnings to understanding its sustainability.

Risk of High Dividend Yield Shares – There is no such thing as free lunch

A segment of the investment population loves high yield dividend shares. But we are always cautious of high dividend yield shares as there is no such thing as a free lunch in the markets. Investors need to ask some critical questions when they see a company with a higher than expected dividend yield. The risks usually fall into the following categories and note these can exist independently or interlinked.

1. The Company’s earnings will be at risk in the future.

An important question is: are the earnings sustainable and can the company maintain the current payout rate? A high yielding stock could mean that the market is already discounting a dividend cut.

2. The market is expecting asset write offs

The company balance sheet’s assets are inflated and the expectation is there will be upcoming write-offs coming and investors looking to get out have sold their shares. The selling pressure depresses the share price and inflates the dividend yield. Note an asset write off can be linked to depressed earnings.

For example, if the market expects real estate prices to fall the investors will sell the ASX REIT shares. Changes to dividends take time to be reflected in the new levels the shares are trading at. We saw the same during the financial crisis. The bank balance sheets were bloated with subprime exposure saw the share price fall way ahead of the subsequent write offs. It is during the period where the write offs are announced where we saw dividend cuts as well.

Everything about dividend payouts

Who declares dividends?

The board of directors manages the company on behalf of the shareholders. This includes hiring and firing the key management leadership team such as the CEO, CFO and COO and other key members of the senior leadership.

Likewise, they are commonly known as agents of the shareholders and it is the role of the board to decide how much of the prior year or historical profit is paid out to shareholders in the form of dividends.

Dividends Payout Policy

There are several ways the board of director can decide how much of earning should be paid as dividends. It is common for directors to decide on a particular policy and communicate it to the shareholders, so the owners and the payout policy remain consistent over time. Dividends can go up and down, but frequent changes in dividend policy show a lack of direction.

Below is a list of dividend payout policies and the board of directors usually chooses a dividend policy that most aligns with the earnings profile.

- Fixed dividend policy – total dividends amount per share paid is fixed year in and year out irrespective of profit cycle. Ideally, cyclical companies adopt a fixed dividend policy to reflect their business’s ups and downs depending on the business cycle. During good times the company underpays its earnings and overpays during recessions. The benefit for shareholders is that this provides a consistent income stream over the cycle.

- Target payout ratio – targeting a specific portion of that year’s profit as dividend. This is an idea of linking shareholder remuneration with the underlying profitability of the business.

- Residual dividend – all profits after the required capital expenditure is distributed to shareholders. Residual dividend policy is frequently adopted by companies that are undergoing a major capital expenditure or reinvestment program. Future dividends can be difficult for management to forecast. Shareholders will receive all excess cashflows after the necessary investment is made.

Dividend Payout Ratio

The dividend payout ratio is defined as the portion of dividends relative to the total earnings for the period. The dividend payout ratio is a proxy of how much of the total earnings are returned to shareholders. Stable and mature companies like the banks, insurance companies and REITs. For these shares the higher payout ratios are rarely cut.

Dividend / Earnings = Payout ratio

Growth companies require a higher rate of reinvestment of the earnings and typically have lower payout ratios. If it pays out the profits, it would either need to raise more equity defeating the dividend’s purpose, raise more debt or forego the growth opportunity.

Overtime as the company matures and the growth rate slows, the board of directors will then shift the payout policy to a higher gear. During this phase, the pace of dividend increase will outpace the earnings growth.

While the payout ratio differs from company to company between industries, companies in the same industry usually have similar dividend payout policies. For example all of the banks will have similar payout policies, while on the other hand, most technology companies offer minimal dividend payouts.

When are dividends paid?

The largest Australian companies by market cap commonly declare dividends every 6 months simultaneously as the half year and annual results announcement. The dividends paid from the half year result is called the interim dividend, and it is usually a bit smaller than the annual dividend.

Once the full year results are announced after the end of the financial year, the company board will declare the annual dividend amount. The final dividend is paid one or two months after the dividend announcement date.

There are no rules which force companies to pay dividends or the frequency of the payments. It is rare for companies to pay monthly dividends due to the administrative cost. Dividends are most commonly paid in 6 months increments because it is the most administratively simple approach as most dividends are still paid by cheque.

Even though quarterly or monthly dividend payments are attractive for investors, the cost of doing it can outweigh the benefits.

Key Dividend Dates

Cum Dividend Date is when the stock owner is still entitled to the upcoming declared dividend.

Ex Dividend Date: This is the last trading date where the investor is entitled to the dividend. As shares are settled Trade+1 days after the trade, the ex dividend date is 1 business day before the record date.

Record Date: The day on which the names on the shareholder register is entitled to the dividend.

Cash Dividend vs Scrip Dividend

Companies in Australia pay cash dividends almost in all instances but can declare a scrip dividend in some rare instances.

What is Scrip Dividend?

Dividend payments can be in the form of cash or company shares which are called scrip. Scrip dividend is when the company issues additional shares to its shareholders as “payment” with the scrip’s value equivalent to the amount declared by the board. Optically this looks like a payment from the company to investors, but there isn’t a transfer of value in reality.

For example, if 100 shareholders each own 1 share in a company and the company declares a scrip dividend of 1 share, each shareholder will own 2 shares. Since the company’s value hasn’t changed, just the total number of outstanding shares by 100. Therefore the value of each share has fallen by 50%.

Another form of scrip dividend is when the company is an investor in another company and makes an in specie distribution. This means passing on its investment to its shareholders.

Dividend Impact on Long Term Returns

Research shows that the value of the dividend makes up a large portion of the total return. In some instances, almost half of the long term return has been attributed to dividends.

Dividend Reinvestment Plan (DRP and DRIP)

Sometimes companies offer an efficient way of reinvesting payouts and this through dividend reinvestment plans commonly known as DRP or DRIP. This allows investors to automatically reinvest dividends without the extra step of going to market and buy shares themselves. DRP plans are put in place at the management’s discretion.

Benefits of participating in DRP

As an incentive for shareholders to reinvest their dividends or participate in these plans, the price of shares issued usually is at a discount to the prevailing trading price. We have seen the average discount for shareholders participating in these plans at around 2.5%. The discount rate can be higher or lower depending on how much the company wants to incentivize the take up rate. Participants also have the benefit of do not have to pay brokerage on the DRP shares.

This page is designed by Dividend Investing as a one stop FAQ on everything important about dividends paid by Australian companies listed on the ASX.

DRP Investing

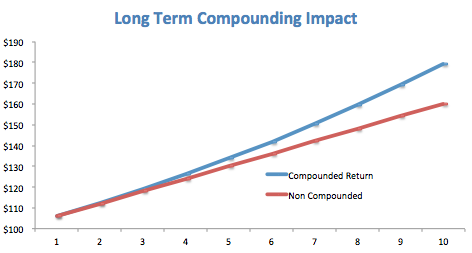

Today’s income can make up the largest investment return component over the long term due to the power of compound interest from the reinvestment of dividends.

The figure below highlights the total return differences between two scenarios: 1) if distribution income is reinvested versus 2) a non-reinvestment scenario over a 10 year timeframe (such as 10 year bonds).

At the end of 10 years, the difference between the 2 lines is 12%. This is from the power of compound interest (assuming both starts at $100 and compounded at 6% over the same time).

The same principle applies to dividend reinvestment plans; however, it is based on the assumption that the share price holds up with any equity risk.

What is an underwritten DRP?

Dividend reinvestment is ultimately a source of equity capital. One weakness of such a source is that it is not a reliable source of capital for companies because it is unpredictable. The amount raised is dependent on the DRP take up rate. To offset this, companies can engage an investment bank to underwrite the DRP plans which is equivalent to all shareholders taking up reinvesting the dividend. These are called an underwritten DRP.

An underwritten dividend reinvestment plan means that the company can reliably depend on the total cash dividend paid out will be returned with any shortfall will be made up by the banks.

Who gets dividends? and Do I get to keep dividends after I sell the shares?

The board will announce in advance a date on which the owners of the shares on that particular date will be able to receive the dividend. Payments are made to shareholders who are owners of the shares on the record date.

If you buy shares, you do not become a shareholder of record until settlement which is T+1 days or 1 day after trading. The dividend is paid to the shareholder on the shareholder register on the record date.

The ex dividend date is the point in time in which the shares are trading without the most recently declared dividend. This is why shares theoretically should drop by the same amount as the dividend on the ex-dividend date.

Franking Credits from Investment

Dividends are covered under the imputation system where the company’s tax is assigned or imputed to the investor as franking credits attached to the dividend. An imputation tax system allows companies to ensure that their profits are only taxed once at the shareholder level. Dividends attached with franking credits are called franked dividends and without franking credits are called unfranked dividends.

This is the biggest benefit of franking credit as the company owners only pay tax once on the income if the tax is paid on the company level, and the investor does not have Double taxation.

Essentially investors only pay income once either at the company level if the company’s earnings are retained to fund future growth or on the individual level if the earnings are passed on to shareholders.

Value of the Franking Credits

The franking credit system prevents the hoarding of cash as management does not excuse saving shareholders from taxes by keeping earnings in the company instead of paying it out.

At the other extreme, as seen in the US, in which the dividends are taxed at the investor and company level. This encourages companies to use share buyback as a primary means of returning capital to shareholders.

Franking Credits Refund

If the investor’s marginal tax rate is lower than the Australian corporate tax rate of 30%, the difference between the fully franked dividend and the investor’s marginal tax rate can be used to offset other income. This is why franked dividends are so popular with retirees and superannuation funds only taxed at 15.

Refund of franking credit can occur even without lodging a tax return by completion by just completing the franking credit refund form on the ATO website.

Australian Franking Credits for Foreign Investors

Only Australian taxpayers benefit from using franking credit when individuals or entities file their tax returns with the ATO. Foreign investors cannot take advantage of the credits if they don’t pay any company taxes in Australia.

Superannuation Franking Credits

The franking credits are especially valuable to superannuation funds due to the tax rate difference between companies and super funds when super funds receive franked dividends to offset other income such as capital gains.

Effectively, the real dividend yield is equivalent to [dividend amount / (1-tax)].

Deferred Tax

Income from listed trusts like Australian Real Estate Investment Trust is called distributions. These investment vehicles are essentially passive investments where the trust collects the income and passing it on to the unitholder. Some of these trusts are structured as staple units where every REIT unit is stapled with a trading corporation.

Franking credits are the resulting tax paid on income from the development or active management of real estate assets. Examples of staple securities included Mirvac and Stockland.

Franking Credit Formula

A franking credit is calculated using the following formula.

Franking Credits= Dividend x (30/70)

Franked Dividend Example

- An investor owns 100 shares in an Australian Company. The company pays $1 dividend per share.

- Income from the company amounts to $100 with franking credits of $100 x (30/70) = $42.85

- The above makes the total income at $100 with an imputation benefit of $42.85.

The implication for investors with the above franked dividend income stream at various tax rates:

- Individuals with expected zero liability will receive $42.85 back from ATO following filing taxes as any taxes already paid is refunded.

- Individuals with 15% tax rate will receive half of the imputation benefit $21.42 as the whole income is taxed at 15%.

- Individuals at 30% tax bracket will keep the $100 in income with no additional tax obligations

- Individuals at the highest bracket will pay the difference between the top income bracket and the embedded imputation credit

Fully Franked Dividend

When the dividend is franked on a 100% basis it is called a fully franked dividend. In the cases of partial franking credits attached to the dividend, the franking portion is simply the percentage times the franked amount.

Grossing Up Dividends

This is best explained by using an example from the last Westpac dividend payment. The last dividend was 80 cents, and it was 100% franked.

A dividend gross up means that on a gross basis for the investor the gross dividend value is 0.80 / 0.7 x 100 where 0.7 is the inverse of the Australian company tax rate for large businesses and 100 is the franking %. The percentage of franking is stated on the dividend statement.

The significance of a dividend gross up is that it represents the dividend’s value on a pre tax basis and allows a direct comparison irrespective of the investment tax structure.

Franking Credit 45 Day Holding Rule

To qualify the benefit of franked dividends, investors must meet the 45 holding rule outlined by the ATO. The rule states that Individuals must maintain ownership or at risk for 45 days. The dates are not inclusive of the purchase and sale dates.

Additionally, if any sale occurs over the period after the dividend has been paid. Investors must maintain more than 30% overall ownership of the original holding.

Small Investors Exemption

Smaller investors are exempt from this rule where over a financial year, total franking credits do not exceed $5000, which is equivalent to $11,666 fully franked dividend amount.

Dividend Withholding Tax

When Australian companies pay a dividend and the owner does not provide a tax file number, they must withhold a certain portion of the dividend amount.

The withholding tax is applied to the gross amount of the unfranked dividend and the amount withheld depends on the ultimate country the investor is located in.

- In countries where Australia has a tax treaty, the dividend withholding rate is 15%.

- In countries where Australia has a no tax treaty, the dividend withholding rate is 30%.

Only residents in that country and beneficiary will benefit from a more favorable dividend withholding regime.

The principal also applies to interest withholding, except the rate is 10%.

If the investor owns a stock of a company listed overseas and if the company paid a dividend. In some instances, the broker is required to withhold a portion of the dividend. The amount withheld will most likely be referred to as dividend withholding tax on the dividend statement.

The same scenario applies to investors owning shares of companies based offshore Australian shares.