Challenger (CGF) share price has taken a beating this year. The market sold off CGF shares following the expectation that interest rates will be lower for longer from now on.

There is not a lot of companies the ASX 200 index with a big moat as Challenger. We like CGF because it is a thematic play on the retirement of the baby boomer generation.

ASX CGF embedded within a growing sector is misunderstood by the market. It contains attractive annuity business and a funds management business that is extremely difficult to replicate.

CGF Dividend Yield

[wpdatatable id=261]

Challenger Dividend History

[wpdatatable id=260]

CGF Dividend Dates

Interim dividends are paid in March

Final dividends are paid in September

What are annuities?

Challenger through its main business Challenger Life is the largest provider of annuities in the Australian market. Annuities provides a steady stream of cash flow over a fixed period or the life of purchaser.

Benefit of annuities versus investing directly in the markets is the shift in investment risk from buyer to the insurer. Essentially the purchaser of annuities mitigates longevity and investment risk in return for credit risk of the purchaser. In return for a certainty of income the purchaser takes a lower return as if they invested in the market directly.

Credit risk for annuity provides is mitigated to an extent through regulation where APRA determines the level of capital required for life insurers and annuity providers.

Challenger in return in issuing the annuity receives the total funds today and reinvest it to earn a higher return and profit from the return it earns and the rate it pays to the buyer.

This is akin to bank lending where the banks earn a spread between their deposits and interest on the loans. Challenger Life’s earnings are the difference between what was promised to the seller and the actual investment return.

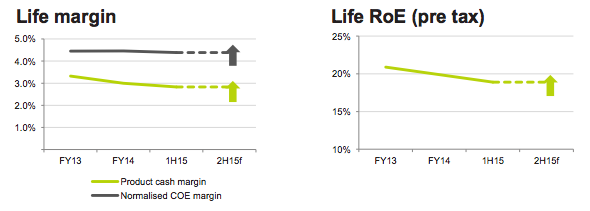

Total return for challenger’s annuity business is predicated on annuity pricing at time of sale which embed a certain return expectation. Chart below highlight the typical margin of the annuity business and the return on equity for challengers life business where typically the annuity business is held.

Key risk of the annuity business is the asset and liability management. The liabilities are the annuity coupon payments with the underlying investment asset income.

The breakdown of asset and liabilities show that in the short term <1 year and 1-3 years. Asset and liabilities are broadly matched.

Annuity Growth Drivers

Challenger annuities business can be broken down between the institution and retail annuity segments. The primary driver of future annuity sales growth is the baby boomer retirement and shift of accumulation of the vast super funds to pension phase.

On the distribution front, it is positive to see the brand recognition it has with advisers. This is also reflected it being on approved product list of all major banks fund management platforms.

Positive to see continue trend into industry super funds to tap that growth market.

Management highlighted the perceived negative impact from the current low RBA cash rate and future annuity sale. Figure below shows volume flows is relatively sticky even under low interest rate environments.

So far underlying Australian annuity sale trend is similar to the US where total annuity sale is not negatively impacted by low interest rates.

Interesting to see if low cash rate actually improve retail book going forward as retirees are less able to be dependent on term deposits and unwilling to take market risk (such as Fixed Income ETFs) and allocate to annuities instead.

Related: Superannuation Calculator to see how much you need to save for retirement

Investment Portfolio

The business prefers long life assets which are severely limited in Australia. This is why it had a mortgage (pre GFC) and debt origination business to source appropriate assets for the life portfolio. This portion are similar to debt investment funds listed on the ASX.

Traditionally it has heavily relied on real estate in its portfolio. The commercial real estate market is being challenged in the post Covid environment and we suspect this is one of the reason why the share price has been sold off heavily during the market sell off and the slow recovery since.