The Sydney apartment prices has consistently traded at a premium to other major capital cities in Australia. We covered the reasons why the geographical constraints of the city will always provide a base level of house and apartment prices in Sydney in a growing population environment. This idea is still applicable even as the current health crisis has temporarily put the brakes on population growth.

The current apartment market is undergoing a period of lull as the uncertainties surrounding the Coronavirus and broader economic weakness is being played out.

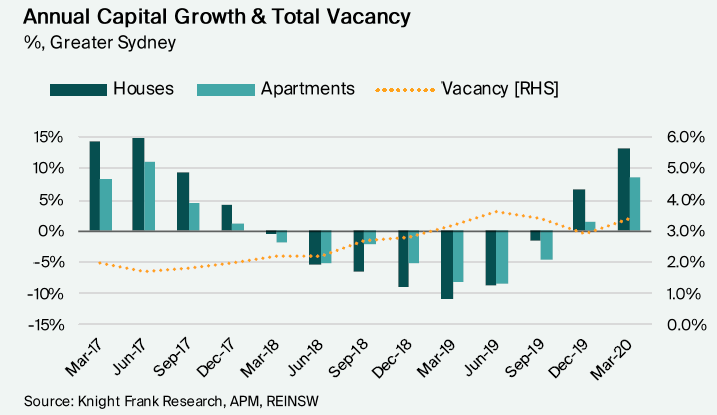

Sydney Apartment Market Up to 2020

The Sydney apartment market was a uncharacteristically weak from 2018 and late 2019. The last cyclical boom in was driven by the low interest rates and strong population growth as result of the end of the mining boom out in the west.

The market reacted to the strong growth via increase in apartment supply and 2018/2019 were the peak years in the apartment deliveries for the projects commissioned during the boom.

Knight Frank has a great chart which captured this trend which shows the quarterly change in the capital values of apartment prices in Sydney.

The market saw a strong recovery in late 2019 and 2020 as supply slowed down and tightening of the bank lending which resulted in only the good products were able to be launched.

All of the signs before the current crisis showed that the residential unit market was being stabilized and could’ve went on a another run.

Is Sydney Apartment Prices going down?

We think Sydney apartment prices will be be lower rather than higher in the next 12 to 24 months. The restriction on inbound tourism and entry of international students puts pressure on the underlying demand.

Both of these factors has severely impacted underlying tenant demand and it is hard to see strong increase in prices when the demand for the products falls through the floor.

Sydney Apartment Supply

While apartment developments will dry up in the next year with the current projects being completed and the forward book of projects basically drying up. The downturn in the tourism sector means the apartment stock which were basically being used by AirBnB as short term accommodation will be converted back for long term rentals.

This coupled with the service apartment operators reshifting their focus to secure long term tenants means that aggregate apartment supply for renting has increased dramatically. This is especially applicable to Sydney due to the importance of both areas to the economy.

The increase in supply in the Sydney market means the weekly rents are already under pressure. This is good for renters as they have more choices and for the first time cheaper accomodation costs. But not an ideal outcome for landlords as they pressure on their income is not a positive sign for the capital value.

Low CBD Apartment Demand

In the same vein on the demand side the limited inflow of international students is also crimping Sydney CBD residential unit prices. Given the southern CBD proximity to the major universities namly UTS, UNSW and The University of Sydney. The lack of student demand means the traditional dependable flow of tenants has dried up for those owners.

Infrastructure Investment to Support Growth

One of the most positive signs for growth however is the continual investment in infrastructure by the government.

The development of the Sydney metro and the expansion of the metro out west and north west provides a strong foundation for growth in new areas.

But it is important to note that see this as more beneficial for the housing stock in general rather than apartment values as they key driver of the metro is improve transport access for areas that were not well serviced by trains.

The completion of the metro will see a revalue of the surrounding land which is characterised by housing as they become potential apartment development sites. Therefore outside of specific areas we see it as a strong positive for Sydney house prices along the train lines and existing units upon completion of the infrastructure projects.

What about the rest of the Sydney Metro market?

Sydney CBD vs Non-CBD Apartments

Generally we see the non CBD markets will do better than the Sydney CBD apartment market. This is due to overall lower level of density where the relative increase in vacancy rates can be absorbed by the existing stock.

The absolute increase in apartment supply in the CBD as result of the above factors cannot be simply absorbed by the current market demand. The cure for is price adjustment on the rents and time for the natural demand to soak up the supply.

The lower density in non CBD markets means although there could be similar level of increase, the absolute levels relative to the total residential stock will not overwhelm the market and the supply can be absorbed in a more management rate.

North Shore

The markets which will outperform are the traditional markets which has always been characterised by limited unit developments. The easiest candidate in this space is the north shore market.

This area has always been dominated by residential demand and a strong culture of NIMBYISM limiting residential supply . The quality of schools, amenities and transport links has always attracted demand in the area and this coupled with limited supply means that any fall in apartment prices in the upper north shore region would be temporary in our view.

Eastern Suburbs

This region is characterised by older stock with the exception of developments near Bondi Junction and Kings Cross. The premium pricing over regular apartments in other sub markets will remain however we expect rents to be under pressure as the market is dominated by young professionals and this is sort of economy where their income growth will be crimped.

The competing alternative is not cheaper rental market elsewhere but moving home back with parents.

Parramatta / Greater Western Sydney

As you would’ve gathered from our view so far, supply is antisis of capital and rental growth. Parramatta is one of the market we see it will flatline for the foreseeable future. The market and outer west region has become a key absorber for the growing Sydney population and this is clearly evident in the developments surrounding Parramatta square.

Given the size of the present and buildable height in the Parramatta CBD there will always be supply of apartment coming to the market in the foreseeable future.

Our Sydney property forecast sees the owning apartment in the Parramatta CBD as comparable to Melbourne CBD / Docklands or Brisbane CBD / Fortitude Valley markets.

There will be capital growth for apartments however whenever the prices get out of hand the increase in supply will price long term appreciation inline with population growth. It is a more slow and steady market rather than a re-rating or secular capital growth story.

Rhodes and Wentworth Point

The last cyclical upswing saw a dramatic increase in Sydney apartment supply and being located in an established market is more beneficial than owning an apartment in a block of apartments surrounded by single or double storey housing.

Greenfields surrounding apartment means there is always a potential for more supply in the future which hampers price growth. A prime example of this is seen Rhodes / Wentworth Point markets.

Market Summary

In sum the above provides some of the key points which we think will drive Sydney apartment capital growth going forward and the impact on some of the major sub markets.

Although the view on the market as a whole, individual apartment values will differ between quality, micro location and emotional sentiment at the time of purchase but we believe the above factors provides a strong baseline trend in which the micro / apartment specific factors which will fluctuate around.