Australia Prudential Regulatory Authority took a proactive role in artificially slowing down bank lending during the last residential cycle peak in 2017/2018 when it intervened in the market directly by requiring the banks to hold higher capital requirements for mortgage loans and instituting total growth restriction of 10% on housing investment lending.

The conservative approach in managing the Australian bank result in the bank shares to underperform the market for a prolonged period of time but ultimately shown to be the right call as the bank balance sheet were unquestionably strong just before Covid.

The primary driver of more stringent lending standard is the risk of a property bubble in Sydney and other major capital cities.

Australian banks responded by raising capital, increased rates on investment loans at first then residential loans independent of changes in interest rates by the RBA and curbing overall appetite to increase investment lending in the housing sector.

We dug around the ABS website for some investment stats and found some useful data points on investment lending that gives some context for the residential lending environment just before the brakes by APRA.

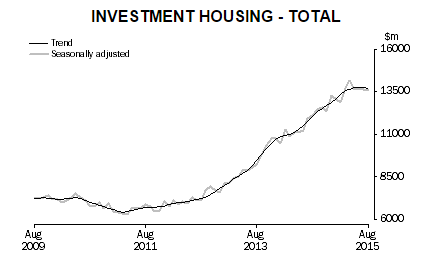

- Total Investment Housing Loan Value

Exhibit 1 above shows the total bank lending for investment in housing since 2009. The eye popping trend is that lending for residential housing has more than doubled since 2011 trough. This is marked parallel to any house price trend since 2009 where prices really took off in the major capital cities.

Banks has dominated bank lending for investment housing since the GFC as the mortgage securitization market and whole sale mortgage markets has been effectively closed.

Historically the cost of debt were higher than the property rental yield. One argument for the increase in investment borrowing overtime is because of potential tax saving from owning negative geared properties.

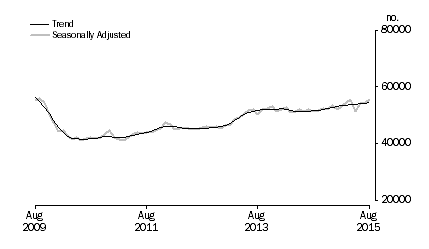

2. Home Owner Occupied Financing

Borrowing by homeowners over the same time shows a more gradual increase. This shows the increase in activity in the residential markets on a incremental basis can be considered to be driven by investors (domestic and foreign).

While the major media focus on foreign investors buying properties in Australia, most are still financed using domestic borrowing rather than pure equity payment for the whole house.

The big 4 banks (like Westpac) has the largest share of investment loan market means that all the exposure sits within the banks balance sheet.

The banks have become concentrated bets on the Australian housing with significant downside risks as any slow down in the economy with job losses would have a magnify impact on bank balance sheet and earnings.

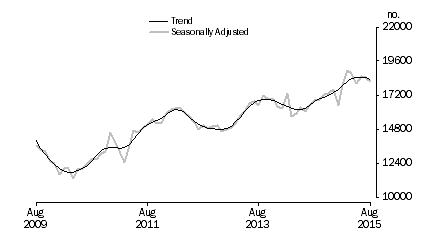

3. Owner Occupied Housing Refinancing

Final table shows the refinancing activity on the home owners in the current RBA rate cut cycle. The trend is undeniably up over the same period where home owners have taken advantage of lower rates by refinancing their mortgage. Interesting to see percentage of homeowners locking in a fixed rate for a set term going forward.

Given the evidence of the strong uptrend in housing lending. We thin the easy money have been made on residential investment in Australia. The next big move potentially could be on the downside. We made a playbook of potential ways to profit from fall in house prices. It is now a matter of timing.